Thought Leadership

Sponsored by Fitch Ratings

2019 Outlook: Commercial Fleet & Truck Leasing and Auto Finance

Fitch Ratings’ 2019 global sector outlook for finance and leasing companies has been revised to stable from negative, as credit losses for consumer finance issuers should remain at the lower end of historical ranges, while commercial finance companies are expected to benefit from generally stabilized residual values and operating environments. This whitepaper provides further details on Fitch’s sub-sector outlooks for commercial fleet leasing, truck rental and leasing and auto finance.

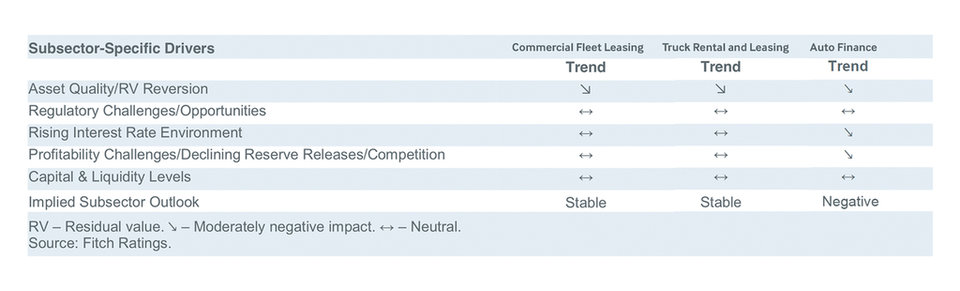

Commercial Fleet Leasing Truck Rental and Leasing Auto Finance

Commercial Fleet Leasing

Used Vehicle Price Pressure to Resume

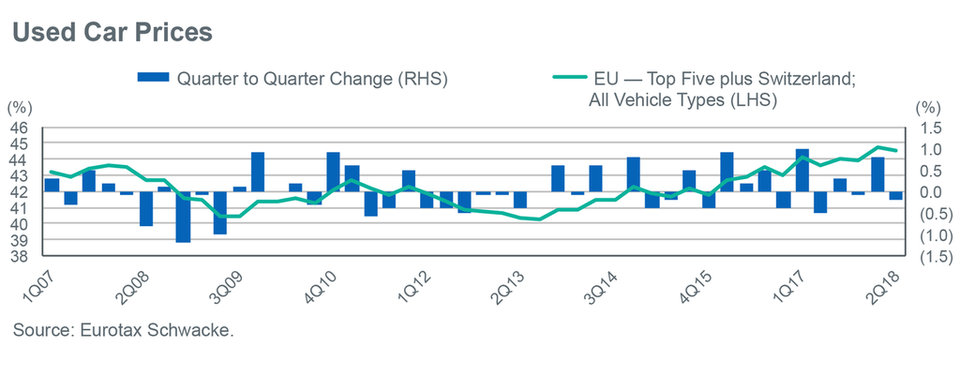

In the U.S., wholesale used vehicle prices have demonstrated strong performance, as evidenced by the Black Book Used Vehicle Retention Index, which ended September 2018 at 116.0, compared with 113.9 one year ago. In the EU, used vehicle prices remain elevated relative to long-term standards, as evidenced by the quarter-over-quarter change in prices for three-year-old vehicles over 24,000 km. Fitch expects downward pressure on used vehicle prices over the medium term, but the impact on earnings should be moderate, particularly for U.S. fleet lessors, which almost exclusively employ open-end lease terms.

Fleet Management Outsourcing Continues

Aside from idiosyncratic credit issues affecting certain issuers, operating performance among commercial fleet lessors in North America and Europe remains supported by consistent core operating cash flows and improved operating leverage. Fitch expects modest portfolio growth for commercial fleet lessors in 2019, driven by increased fleet management outsourcing due to the rising costs and complexity of maintaining fleet ownership.

Manageable Interest Rate Sensitivity

Fitch views commercial fleet lessors as having a relatively less cyclical business model than other large equipment lessors since they have a greater focus on essential services and benefit from a shorter order-to-delivery cycle. Interest rate sensitivity for commercial fleet lessors is relatively limited, as lessors seek to mitigate this risk by issuing term debt to match-fund lease terms. In the case of shorter-term lease or rental contracts, firms have the ability to pass on higher funding costs to customers in lease rates relatively quickly.

Truck Rental and Leasing

Strong Freight Demand to Support Rental Revenue

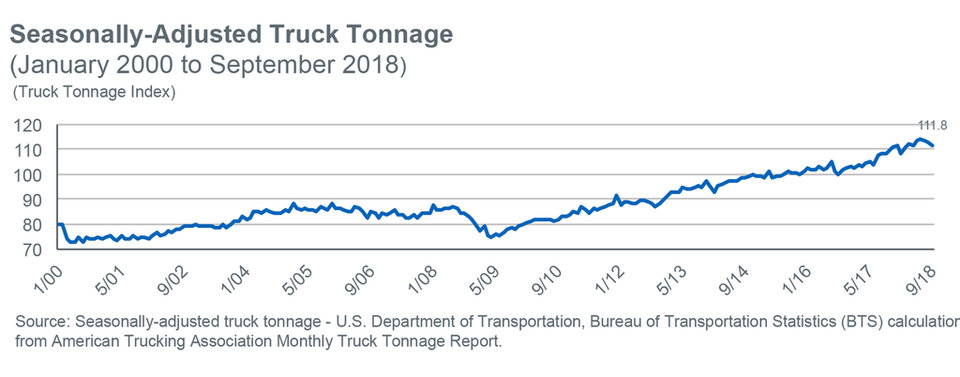

According to the American Trucking Association’s truck index, freight demand in the U.S. remains on a long-term upward trajectory, with tonnage up 7.0% through September 2018,year over year. Continued growth in freight demand was driven by solid manufacturing, retail sales and construction activity, compounded by structural challenges such as continued driver shortages and regulations limiting hours of service. Fitch expects current freight demand to drive continued growth in truck lessors’ commercial rental revenue in 2019.

Discretionary Vehicle Replacement to Drive Negative Free Cash Flow

Heavy-duty truck sales are nearing record highs given strong freight demand, higher cargo rates and the desire of carriers to enhance the performance and efficiency of their operations with newer technology equipment. Truck lessors are expected to contribute to the growing manufacturer backlog to replace older vehicles and grow their fleets. As a result, Fitch expects free cash flow will be negative in the near term, although truck lessors have the flexibility to curtail these capital expenditures and strengthen free cash flow in the event of a downturn.

Stable Used Truck Environment Expected

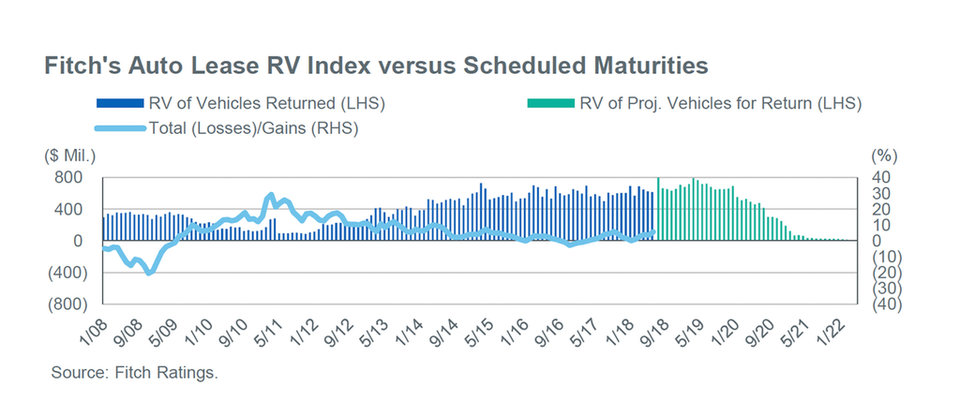

Lessors have experienced below-average residual value gains over the past three years. For example, the residual gain rate for the 12months ended2Q18 was 11.1% for the two publicly rated truck lessors, compared with an average of 20.5% since 2011. Fitch believes rated truck lessors maintain appropriate depreciation policies and have established track records for vehicle disposition due to their emphasis on vehicle maintenance and quality. Fitch believes the used truck environment will be stable for 2019, as improved pricing on used vehicles will be offset by growing used-vehicle inventory from replacement demand.

Auto Finance

Credit Performance Crosscurrents Remain

Credit performance in the U.S. auto finance sector has stabilized over the past year, driven by a strengthening macroeconomic environment highlighted by historically low unemployment and improving personal income growth supported by the federal tax cuts. Credit performance has also benefitted from a tightening of underwriting standards in 2017. However, rising consumer debt burdens, higher interest rates, elevated off-lease vehicle supply and further extension of loan terms could lead to weaker credit performance in 2019.

Used Vehicle Prices Stabilize in 2018, But Face Further Pressure

Contrary to expectations for declines, used vehicle prices stabilized in 2018, according to both J.D. Power Valuation Services and Black Book used vehicle indices. Fitch believes the improvement is attributable to a multitude of factors, including a strengthening U.S. economy, a widening cost differential between new and used vehicles, and greater discipline on the part of OEMs in managing vehicle inventory. Nonetheless, Fitch expects used vehicle prices to come back under pressure as off-lease vehicle supply rises further in 2019.

Profitability Challenges Drive Negative Subsector Outlook

While the relative strength of key macroeconomic indicators will be a primary driver of loan growth and credit performance for the auto finance sector in 2019, Fitch believes the competitive environment will intensify with certain banks resuming growth and credit unions continuing to gain market share. Rising interest rates will pressure net interest margins to varying degrees, as auto loans are largely fixed rate, depending on the issuer’s funding mix.

Fitch Ratings