COMMENT

Obstacles on the road to a low-carbon future

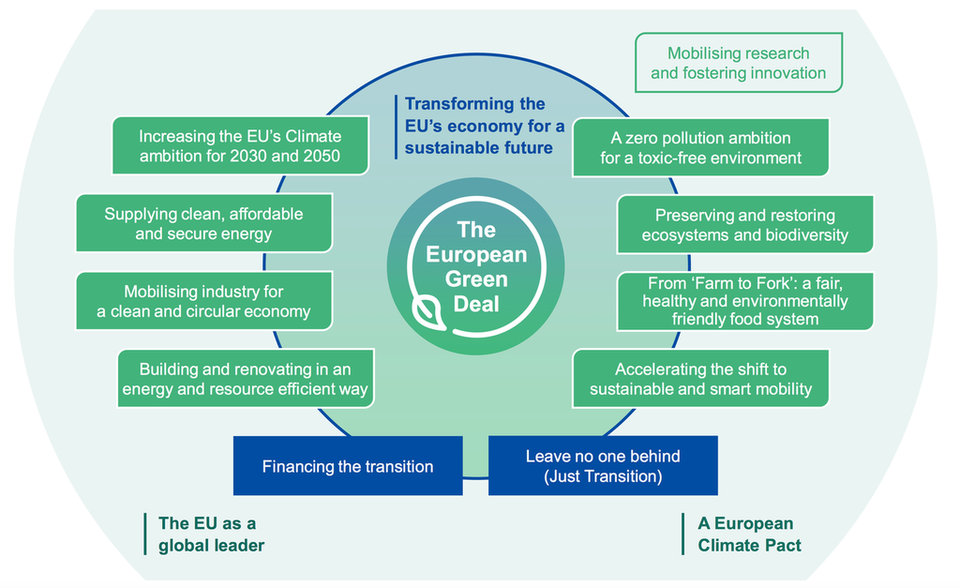

Earlier this year, the European Union (EU) outlined its plan to tackle the ecological crisis and the economic crises together by pledging to put a Green Deal at the centre of a €750bn post-pandemic economic recovery plan, but without a more solid commitment to ending the funding of new fossil fuel projects, banking reform may be necessary if climate disaster is to be averted. Alejandro Gonzalez reports.

Image: Chrispictures

During her first State of the Union address in September, EC president, Ursula von der Leyen, unveiled plans to increase the EU’s 2030 target for emissions reduction from 40% to 55%, to put the EU on track for climate neutrality by 2050.

But, even if EU legislation is successfully introduced to meet these obligations by the end of summer 2021, there are other reasons to be sceptical about the EU’s ability to deliver on its green agenda.

Clearly, for this plan to succeed, big banks will need to come on board in a big way.

According to the European Banking Federation, the trade association that represents 32 national banking associations in the EU and EFTA countries, banks are crucial to ensuring the success of a Green Deal as they will, “play an essential and pivotal role in financing the change to a sustainable economy.”

What is a major concern though is that Europe’s major banks appear to be continuing to invest very large sums in the fossil fuel industry, even after signing the 2015 Paris Climate accord.

Research by BankTrack and the Rainbow Action Network, two NGOs that monitor private sector banks, reported in March 2020 that 35 of the world’s largest banks have together funnelled US$2.7 trillion into fossil fuels in the four years since the Paris Agreement was adopted (2016 to 2019).

Of the European banks cited in its Banking on Climate Change report, Barclays was the largest supporter of fossil fuels followed by HSBC, during these four years.

The report also identified HSBC, Santander, BNP Paribas, Crédit Agricole, Deutsche Bank and Societe Generale (some of Europe's top bank asset leasing companies) as lead underwriters for the December 2019 IPO of Saudi Aramco, the world’s largest oil producer.

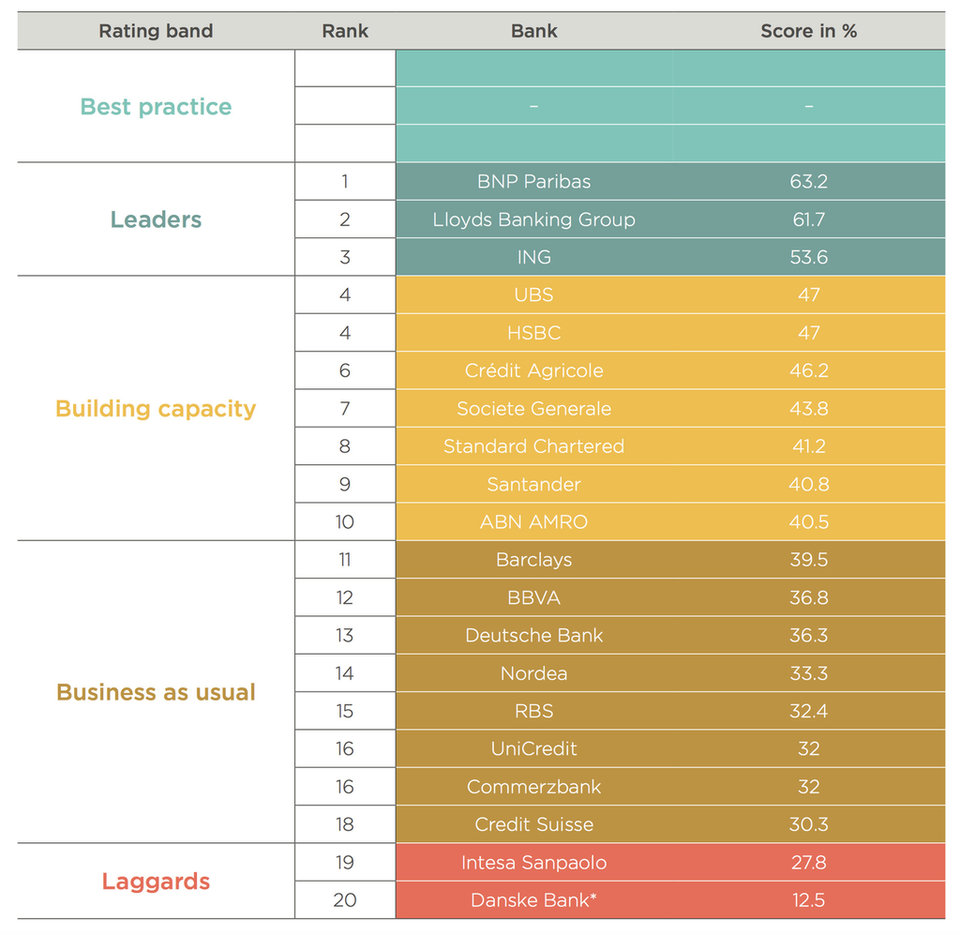

More recently, ShareAction, a London-based charity that promotes responsible investment, ranked Europe’s top 20 listed banks on their responses to climate change. Its latest report, Banking on a Low-Carbon Future II, published in April 2020, is based on information from December 2019.

To arrive at its ranking, ShareAction applied the Task Force on Climate-Related Financial Disclosures (TFCD) recommendations for banks.

The TFCD was established by the G-20 Financial Stability Board in 2015 to encourage the disclosure of consistent climate-related financial information.

ShareAction scored banks on how they responded to a questionnaire covering four themes:

· Climate-related risk assessment and management (35%)

· Low-carbon products and services (35%)

· Public policy engagement and collaboration with other actors (15%)

· Governance, strategy and implementation (15%

Report card

In issuing its report card for the sector, ShareAction said European banks are “not yet doing enough to tackle the climate crisis,” with a group average of just 39.9%.

“Not a single bank currently represents best practice in managing climate-related risks and opportunities across all assessed areas,” the author of the report said.

Generally speaking, “the banks’ policies in relation to high-carbon sectors are currently still insufficient to ensure alignment with the goals of the Paris Agreement, and often they are just tinkering around the edges.

“While banks have largely stopped providing project finance for coal mining and coal power, policies on general corporate financing for companies reliant on coal are still missing.

“Similarly, some banks have started to introduce exclusions for some forms of unconventional oil and gas, but policies on conventional oil and gas are lacking.

"There is a real risk that banks’ continued financing of fossil fuels will overshadow any positive impacts they might achieve through financing low-carbon solutions.

“Despite the range of barriers to green finance identified by the surveyed banks, all banks appear to be actively looking to scale up green financing and develop low-carbon products and services,” according to the report.

BNP Paribas, among Europe's top bank asset finance earners, scored the highest thanks to its consultation with stakeholders about their priorities and its decision to exclude non-conventional oil and gas financing of tar sands and arctic drilling.

Other significant European bank lessors, by turnover, include: Lloyds Banking Group, ING, HSBC, Credit Agricole, Societe Generale, Santander and ABN AMRO, all of which find themselves in ShareAction’s top 10.

Lloyds, which came last of 20 in ShareAction’s 2017 survey, was ranked second this year, demonstrating that “it is possible to improve climate-related performance very quickly,” the report says.

Lloyds is “the first surveyed bank to have set an ambitious numeric target to reduce the carbon intensity of its lending activities,” the report adds.

ShareAction also noted that:

· Societe Generale has committed to deliver €120bn in financing for energy transition between 2019 and 2023, updating their prior target of €100bn between 2016 and 2020.

· BBVA has made a more general sustainable finance pledge of €100bn between 2018 and 2025.

· ING is committed to reducing its exposure to coal power generation and coal mining to close to zero by 2025. “This means that by the end of 2025, ING will no longer finance companies in the utility sector more than five per cent reliant on coal-fired power in their energy mix,” the report said.

Intesa Sanpaolo

ShareAction ranks Italian banking group Intesa Sanpaolo, a notable provider of asset finance, coming in 12th in Asset Finance Policy’s 2019 ranking of Europe’s top 50 asset finance providers, as one of its laggards.

But not all ESG experts see the group in the same light.

In a statement, the bank said: "Intesa Sanpaolo ranks at the top of the main sustainability indices such as the MSCI ESG Score, the Bloomberg ESG Disclosure Score and the CDP Climate Change Score.

"Intesa is also the only Italian bank listed in the Dow Jones Sustainability Indexes, the CDP Climate A-List 2019 and the 2020 Corporate Knights Global 100 Most Sustainable Corporations in the World Index.

"The 2020 Institutional Investor ranks Intesa Sanpaolo as Europe's best bank for ESG practices. In January, Intesa Sanpaolo committed to providing €50 billion in new lending dedicated to the EU’s European Green Deal.

"In 2018, the bank launched a €5bn circular economy financing facility that has already disbursed €1.5bn, of which €740m in the first 9 months of 2020," the bank said.

Intesa Sanpaolo made its first international investment in the circular economy with a £175m (€200m) finance agreement with Thames Water in 2019.

“Thames Water will be incentivised to meet targets based around adopting circular economy principles which, if met, can unlock improved finance terms,” according to an August 2020 report entitled Green Asset Finance: A New Business Landscape by the Helsinki-based IT company TietoEVRY. A second international deal followed this year to finance Germany’s GreenCycle.

In 2019, Intesa Sanpaolo’s disbursements for the green and circular economy totalled around €2.2bn, equal to 3.7% of total loans. This brought Intesa’s 10-year total to about €20bn.

But according to the bank’s consolidated non-financial statement, as at 30 June 2020, loans disbursed for the green and circular economy in the first half of 2020 were “approximately €780m disbursed, equal to 1.9% of total loans.” The bank says that green disbursements this year were negatively affected by the Covid-19 pandemic.

Green legislatures

Clearly without improvements by European banks in climate-related risk assessment, innovation in low-carbon products and services, better public policy engagement and a commitment to a green strategy and its implementation, the success of the EU’s vast decarbonisation programme cannot be guaranteed.

If the 2050 targets are met, observers say Europe will become the first climate neutral bloc in the world, and will be positioned as the global frontrunner in tackling climate change, thereby allowing asset finance and leasing to help make this a reality. But if boardrooms continue to be too slow to respond to change in the face of overwhelming evidence of a heating planet, legislatures will be left with few options but to enact popular bank reform agendas.

Close Brothers

Fitch said the fallout from the pandemic “has heightened risks to the group given its above-average exposure to SME lending through asset and invoice finance, to retail customers potentially affected by employment disruptions in motor finance, and to property lending that will suffer delays in completion and sales.”

It said the ratings of Close Brothers Group and Close Brothers Limited “reflect a strong record of performance through economic cycles, which has historically compensated their appetite for higher-risk lending” but added that in the current crisis, “we expect pressure on earnings through rising credit impairments and lower volumes.”

Investec Bank

Fitch said its action on Investec Bank plc (IBP) reflects the fallout from the pandemic crisis “represents a near-term risk to its ratings”.

It said: “The risks stem from the bank’s above-average exposure (as a proportion of gross loans) to sectors we consider as particularly vulnerable to disruption, such as small-ticket asset finance, aviation finance, corporate and acquisition finance.”

Metro Bank

The rating action taken by Fitch reflects heightened challenges to Metro Bank’s business model, earnings and ability to deliver its strategy, which the pandemic has added to.

It said: “The coronavirus disruptions make execution on Metro Bank’s strategy more difficult in the near-term because of weaker prospects for growth, lower interest rates, and slower demand for loans.

“The bank has been undergoing significant organisational changes, and its earnings were expected to be depressed by restructuring charges and a slowdown in lending.

“The pandemic also poses an operational challenge for Metro Bank given its small size, staff capacity and management turnover.

“Metro Bank’s earnings are very weak (£53m operating loss in 2019, excluding the impairment of tangible and intangible assets).

“Fitch expects that a return to profitability will be made more difficult by the coronavirus disruptions. Lower lending volumes, interest rates and transaction fees, and larger credit losses (from small amounts) will weigh on the 2020 loss.”

Paragon Bank

Fitch said Paragon had “a good record in maintaining sound asset quality and profitability, but we expect its businesses, particularly its SME and development finance business, but also buy-to-let (BTL) mortgage lending, to be at risk from asset non-performance and reduced profitability in the downturn.

“We also believe that funding growth at Paragon Bank will be harder to achieve, given possible pressures on saving rates if unemployment increases, and that the bank will find it harder to execute its strategy.”

The Co-op Bank

Fitch said the downgrades of the Co-operative Bank “reflect our view that the economic disruption in the UK poses a material risk to the bank’s capitalisation and earnings, as well as to the stability of the business model and to management’s ability to execute on its strategy to grow revenue and return to profitability, relative to when we last reviewed the ratings.”

“The bank enters the economic downturn from a position of relative weakness given its structurally loss-making profile. The bank is vulnerable to greater-than-expected losses and continues to face challenges in its ability to execute its future strategic initiatives.

“We also see a heightened risk of asset-quality deterioration, although this is partly mitigated by the secured nature of its loan book.

Virgin Money

Fitch the fallout from the pandemic “results in heightened risks to Virgin Money UK’s ratings since the bank enters the economic downturn from a position of relative weakness given its weak profitability compared with peers’ as the business continues to undergo restructuring following its 2018 merger.”

“We have reflected the highly likely impact of the economic and financial market fallout from the pandemic in a weaker assessment of earnings relative to when we last reviewed the bank’s ratings.

“We also see an increased likelihood of future asset-quality deterioration, particularly in SME lending and credit cards, as well as weaker capital generation,” the agency reported

Banks’ asset finance business operations

- Investec Bank has a subsidiary, Investec Asset Finance plc

- CYBG-owned Virgin Money plc runs an asset finance division

- Close Brothers Group plc operates an asset finance division

- Metro Bank plc operates two subsidiaries: SME Asset Finance Limited and SME Invoice Finance Limited

- The Co-Operative Bank plc runs its leasing through various subsidiaries (Second, Third and Fourth Roodhill Leasing Limited)

- Paragon Bank plc runs an asset finance division

GO TO TOP

Share this article