SHIP LEASING

Hong Kong enacts new ship leasing concessions

Hong Kong’s new tax incentives for ship leasing are part of an initiative to re-energise its maritime industry, after the container port – once the world’s busiest – slipped to 8th place on declining volumes last year. Katherine Muir reports.

Image: Chrispictures

Hong Kong recently introduced new tax breaks for ship leasing as part of its plans to grow its global market share of the industry along the ‘Maritime Silk Road’.

The new tax break states that qualifying profits of ship lessors carrying out operating lease and finance lease activities, such as sub-leasing and sale and leaseback arrangement, will see a tax rate of 0%.

Meanwhile, the tax rate on the qualifying profits of ship leasing management activities for ship lessors for associated and non-associated companies will be 0% and 8.25% respectively. This new tax regime will be applicable to revenue received either on or after 1 April 2020.

Hong Kong ship leasing

The move reflects Hong Kong’s aims to position itself as a global centre for ship financing and leasing, building on its reputation as a major shipping hub.

Hong Kong has long been an attractive regional base for the shipping industry, due to its status as a global financial centre, its world-class port, dynamic workforce and competitive tax regime, as well as its proximity to Asia’s major markets.

As a result of this, a thriving maritime sector operates in the territory, from maritime financiers, insurers, lawyers and arbitration services to shipbrokers, insurance companies and cargo operators.

Tim Huxley, the founder of Mandarin Shipping, described the local industry conditions to the South China Morning Post as: “The full range of services to build, operate, register and insure a ship are all within walking distance here in Hong Kong.”

There have been major changes affecting the port over last decade, however, with big shifts in the financing of shipping since the financial crisis of 2008, when the industry’s traditional financiers – the European banks – largely withdrew from the market.

This has led to less conventional sources of funding stepping in including American private equity funds and Chinese and Japanese leasing firms, according to the Hong Kong Maritime Hub website, which profiles the territory’s maritime sector, listing Chinese companies such as ICBC, Bank of China, Bank of Communications, China Construction Bank, and Minsheng Financial Leasing as having moved into ship leasing, and now dominate the shipping market in East Asia.

This change has coincided with the territory’s maritime services industry being challenged by other regional players, such as Singapore, which has led to its slip down the international rankings of global shipping.

The change is reported to be partly due to a shift away from manufacturing towards financial services in the territory.

However, as part of the Chinese government’s multibillion-dollar Belt and Road initiatives (the ‘road’ refers to sea routes), including the Greater Bay Area project, Hong Kong’s maritime sector is now assuming more importance again.

In 2017, the government introduced a concessionary tax regime to attract more aircraft leasing companies to set up in Hong Kong, reducing the profits tax of qualifying aircraft lessors and aircraft leasing managers.

This move fuelled the maritime sector to ask for a similar tax break, with the Hong Kong Financial Services Development Council calling for tax concessions such as a reduced rate of 8.25% “where relevant businesses activities such as maritime and ship leasing management and maritime and shipping-related supporting services activities are carried out in Hong Kong”.

The government’s discussion paper on the proposal to introduce the new tax regime noted that the global shipping fleet has largely grown at a rate of 3% per annum between 1980 and 2018, and is expected to continue growing, with the Financial Services Development Council estimating in May 2018 that: “the capital expenditure for new-building vessels was about US$80-100bn a year”.

The discussion paper also pointed out that the OECD’s tightening of international taxation rules to deal with tax abuses, particularly anti-base erosion and profit shifting (“BEPS“) measures, had driven ship leasing companies based in low-tax countries to look for opportunities to rebase their operations, giving Hong Kong an opportunity to attract new business to the territory.

Qualifying lessors

The resulting legislation states: “Qualifying ship lessors and leasing managers will still be taxed such that issues relating to BEPS and related anti-tax avoidance will not be an issue and interest received under a finance lease will also be subject to tax,” as cited in a recent paper exploring the issue by the law firm the Maples Group.

The group also looked at who qualifies for the concessions writing: “To qualify as a ship lessor, the entity must not only be established in Hong Kong but also maintain at least two full-time employees with a minimum operating expenditure of approximately US$1m for the relevant tax year.

“Likewise, to qualify as a ship leasing manager, the Hong Kong-based entity must maintain at least one full-time employee in the Territory and have at least US$130,000 in operating costs. In both cases, the conditions must also be ‘adequate’ in the opinion of the Inland Revenue department itself.”

Benjamin Wong, head of maritime cluster of Invest Hong Kong, Government of the Hong Kong Special Administrative Region, told Seatrade Maritime News in August: “For ship leasing, the [Hong Kong] government is actually planning or forecasting that in 10 years’ time we should be able to capture about 12% of the world’s market – something we are quite confident about.

“In terms of the gravitational pull from shipping and ship leasing, they are much stronger than aviation.

“Hong Kong also has a strong financial market to support leasing activities and we are confident that we can be as successful, if not more successful, than our aircraft leasing”.

Bill Guo, executive director of shipping at ICBC Leasing, told Seatrade Maritime News: “With the new tax scheme, we can and could do more in Hong Kong, including setting up subsidiary companies.

"It’s a good opportunity for mainland Chinese companies to access more talented people in Hong Kong, as the majority of Chinese leasing companies are now based in Beijing, Shanghai and Shenzhen.”

Rosita Lau, a partner at Ince & Co, told the news service about the “retrospective effect” of the tax regime. “If profits earned from that day [1 January 2020] had been in compliance, then you can enjoy the new tax concessions,” she said.

The government tax break, the Inland Revenue (Amendment) (Ship Leasing Tax Concessions) Ordinance 2020, came into effect on 19 June 2020, installing concessionary tax regimes for qualifying ship lessors and ship leasing managers.

Katherine Muir is a freelance journalist

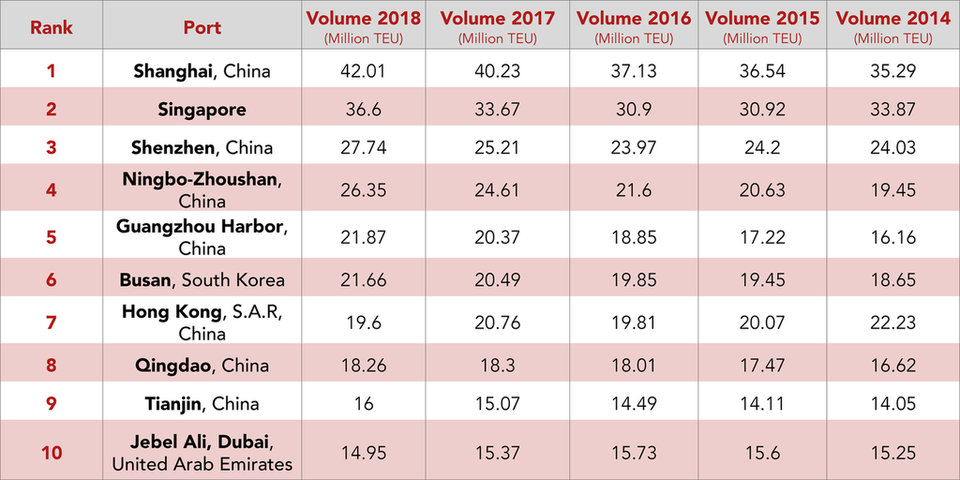

Top 10 world container ports

Source: World Shipping Council

Close Brothers

Fitch said the fallout from the pandemic “has heightened risks to the group given its above-average exposure to SME lending through asset and invoice finance, to retail customers potentially affected by employment disruptions in motor finance, and to property lending that will suffer delays in completion and sales.”

It said the ratings of Close Brothers Group and Close Brothers Limited “reflect a strong record of performance through economic cycles, which has historically compensated their appetite for higher-risk lending” but added that in the current crisis, “we expect pressure on earnings through rising credit impairments and lower volumes.”

Investec Bank

Fitch said its action on Investec Bank plc (IBP) reflects the fallout from the pandemic crisis “represents a near-term risk to its ratings”.

It said: “The risks stem from the bank’s above-average exposure (as a proportion of gross loans) to sectors we consider as particularly vulnerable to disruption, such as small-ticket asset finance, aviation finance, corporate and acquisition finance.”

Metro Bank

The rating action taken by Fitch reflects heightened challenges to Metro Bank’s business model, earnings and ability to deliver its strategy, which the pandemic has added to.

It said: “The coronavirus disruptions make execution on Metro Bank’s strategy more difficult in the near-term because of weaker prospects for growth, lower interest rates, and slower demand for loans.

“The bank has been undergoing significant organisational changes, and its earnings were expected to be depressed by restructuring charges and a slowdown in lending.

“The pandemic also poses an operational challenge for Metro Bank given its small size, staff capacity and management turnover.

“Metro Bank’s earnings are very weak (£53m operating loss in 2019, excluding the impairment of tangible and intangible assets).

“Fitch expects that a return to profitability will be made more difficult by the coronavirus disruptions. Lower lending volumes, interest rates and transaction fees, and larger credit losses (from small amounts) will weigh on the 2020 loss.”

Paragon Bank

Fitch said Paragon had “a good record in maintaining sound asset quality and profitability, but we expect its businesses, particularly its SME and development finance business, but also buy-to-let (BTL) mortgage lending, to be at risk from asset non-performance and reduced profitability in the downturn.

“We also believe that funding growth at Paragon Bank will be harder to achieve, given possible pressures on saving rates if unemployment increases, and that the bank will find it harder to execute its strategy.”

The Co-op Bank

Fitch said the downgrades of the Co-operative Bank “reflect our view that the economic disruption in the UK poses a material risk to the bank’s capitalisation and earnings, as well as to the stability of the business model and to management’s ability to execute on its strategy to grow revenue and return to profitability, relative to when we last reviewed the ratings.”

“The bank enters the economic downturn from a position of relative weakness given its structurally loss-making profile. The bank is vulnerable to greater-than-expected losses and continues to face challenges in its ability to execute its future strategic initiatives.

“We also see a heightened risk of asset-quality deterioration, although this is partly mitigated by the secured nature of its loan book.

Virgin Money

Fitch the fallout from the pandemic “results in heightened risks to Virgin Money UK’s ratings since the bank enters the economic downturn from a position of relative weakness given its weak profitability compared with peers’ as the business continues to undergo restructuring following its 2018 merger.”

“We have reflected the highly likely impact of the economic and financial market fallout from the pandemic in a weaker assessment of earnings relative to when we last reviewed the bank’s ratings.

“We also see an increased likelihood of future asset-quality deterioration, particularly in SME lending and credit cards, as well as weaker capital generation,” the agency reported

Banks’ asset finance business operations

- Investec Bank has a subsidiary, Investec Asset Finance plc

- CYBG-owned Virgin Money plc runs an asset finance division

- Close Brothers Group plc operates an asset finance division

- Metro Bank plc operates two subsidiaries: SME Asset Finance Limited and SME Invoice Finance Limited

- The Co-Operative Bank plc runs its leasing through various subsidiaries (Second, Third and Fourth Roodhill Leasing Limited)

- Paragon Bank plc runs an asset finance division

GO TO TOP

Share this article